July 11, 2005

Movie Economics: Quote of the Day

"Shot on budgets ranging from $1 million to $2 million, Sci Fi's movies are made in money-saving locales like Bulgaria, Romania and Missouri."

June 18, 2005

Pontiac Solstice: Dealers vs. GM

Ever so often the "dealer system" is revealed to be a strangely organized, unruly, complicated mess, as when it sets up incentives for dealers (agents) to interfere with the planned maximization of net present value for the whole company:

GM's performance brand already has piled up 9,000 orders for the sporty ragtop, about half the number it had planned to build this year.But GM already took that risk; I simply cannot believe that they didn't think of this ahead of time.But instead of celebrating, Pontiac is quietly -- and delicately -- addressing complaints that its dealers are asking "well above" the $19,995 base sticker price for Solstice, according to a memo sent to Pontiac's 2,700 U.S. dealers....

Pontiac contends that Solstice's $19,995 base price, including destination fees, is a crucial piece of its marketing efforts and that the rebounding brand cannot risk alienating buyers with inflated prices.

June 09, 2005

The CPI does NOT Measure Prices

Because the cost of housing is imputed through housing rental markets, and because hedonic regression quality-change adjustment, the CPI is now alleged to understate inflation:

If you believe that the CPI is supposed to measure such a thing, then this housing argument appears right on target...

Home prices in the Washington area have doubled or tripled in many neighborhoods, and the cost of maintaining, heating, cooling and improving homes also has been soaring....

Yet the department's housing cost index rose only by 2.7 percent in the past year a discrepancy that has economists scratching their heads.

"The core CPI considerably misrepresents what is happening in the housing market," said John Silvia, chief economist at Wachovia Securities, who added it's "time to can the core."

The problem with the housing index, economists say, is it does not measure the cost of owning a home but rather reflects the cost of renting, which has been rising much more slowly than the cost of home purchases and upkeep.

And what the BLS says about "rental equivalence" is that owners equivalent rent is approximately 22% of the total CPI, and is a sample of renters adjusted to meet the characteristics of nearby owned houses.

Clearly, when housing prices rise but rents don't there is a negative bias in OER. Similarly, when rents rise, but housing prices don't there's a positive bias in OER.

But wait a second, aren't we in a speculator-induced bubble in housing caused by low interest rates? Most people buy homes with mortgages. The monthly cost of owning a home is more than the pro-rated purchase price; it's really the size of the mortgage payment (principal and interest), utilities, and taxes. The core CPI doesn't adjust for lower interest rates and new-fangled interest-only loans either.

As Barry Ritholtz notes, lower interest rates correlate with lower owners equivalent rent through impacts on the demand for house-ownership. Barry considers this a negative bias in the CPI, but I consider this an appropriate adjustment for the lower cost of ownership due to lower interest rates.

The CPI misses the increase in prices, but it also misses the decrease in interest rates. Which is the greater impact on out of pocket costs probably depends on where you live... Compare Santa Monica, CA to Buffalo, NY... Up-to-date data on U.S. fixed and variable mortgage interest rates paid, sizes of mortgages, and sales prices can be found at the Federal Housing Finance Board.

If you haven't had enough housing price talk, you can visit the housing bubble blog.

The rest of the WaTimes article is just one big muddle about too much quality adjustment. But it never defines what the CPI measures, what is meant by "inflation", and how and why this differs from the prices people actually see.

The CPI does not measure "out of pocket" costs, and so if it is underestimating those costs, the fault really lies with the person using the data inappropriately, not with the BLS.

The point is that, yes, non-housing consumer costs are rising, but so are consumer benefits. The CPI is not measuring the change in gross cost to purchasing a thing called a television set, or a computer, or an automobile. It is measuring the change in cost net of change in benefit. It does not try to measure just the increase in the prices people pay, but also the quality and configuration of the goods people are buying.

If you want to gauge out-of-pocket costs, then perhaps you should look at data that actually tries to perform that task.

There is, of course, a very simple solution to this problem. Have the BLS produce a specalist "research" index that doesn't use hedonic indexing or quality adustment at all...

April 08, 2005

Slotting Fees are Efficient (or Maybe not)

Via Progressive Grocer, we find an empirical study that supports the hypothesis that slotting fees -- extra payment for the best shelf space in a retail stores -- are "efficient":

The authors of the report, "Are Slotting Allowances Efficiency-Enhancing or Anti-Competitive?", said they obtained a unique data set consisting of all new products that were offered to a large supermarket chain in a six-month period. It captures more than 1,000 product offers in 21 categories, from major manufacturers such as Kraft, General Foods, Procter & Gamble, as well as smaller manufacturers such as Seneca Foods.Here's a copy of the paper. An abstract of the abstract:The researchers, K. Sudhir of the Yale School of Management and Vithala R. Rao of Johnson Graduate School of Management at Cornell, maintained that the lack of empirical research on slotting allowances prior to their project was due in part to the difficulty in getting retailers and manufacturers to part with information about these transactions....

"We find that when retailers perceive that a product is likely to be a sure hit, they don't seem to ask for slotting allowances; further, manufacturers don't offer slotting allowances when they perceive the product to be a sure dud, either, because they are unlikely to recover the money from sales," said Sudhir.

"It is in the unknown middle, when uncertainty about product success is greatest, that slotting allowances offer the maximum benefit to obtain retail shelf space," according to Sudhir, adding, "This flies in the face of arguments that slotting allowances are merely a form of extortion by retailers."

Using data on all new products that were offered to one retailer for a period of six months, we

empirically investigate support for the alternative rationales for slotting allowances. Our analysis indicates that broadly there is more support for the efficiency theories than for the anticompetitive theories. We find evidence that slotting allowances (1) serve to efficiently allocate scarce retail shelf space; (2) help balance the risk of new product failure between manufacturers and retailers; (3) help manufacturers signal private information about potential success of new products and (4) serve to widen retail distribution for manufacturers by mitigating retail competition. We find little support for the anti-competitive rationales in our data. The fact that we find support for the efficiency rationales suggests that the FTC was correct in being circumspect about banning slotting allowances outright.

UPDATE: Read about contrary views on ALP.

January 05, 2005

More on Drug Reimportation: Price Convergance

The massive discounts on drug prices in Canada don't appear to be too sticky.

Americans purchasing their drugs from Canadian online pharmacies didn't save as much money last year as they did in 2003, with the average discount dropping to 29 percent from 38 percent, a new study found.The average drug price on Canadian Internet pharmacies rose 23 percent from the first quarter of 2003 until the end of last year. Meanwhile, drug prices at American online pharmacies rose 8 percent, according to PharmacyChecker.com, which tracks Internet pharmacy prices and released the study.

Apparently the efforts to block exportation to the US were tighter than I had thought:

To circumvent the restrictions and keep supplying their American customers, Internet pharmacies have been buying drugs from Canadian brick and mortar drug stores, which charge them a markup of between 7 percent and 15 percent above wholesale prices. The higher acquisition costs combined with being paid with weak American dollars is hurting Internet pharmacies' profits."This has become a really low margin business for us," said David MacKay, executive director of the Canadian Internet Pharmacy Association. "We are just trying to hang on."

The comment about the weak dollar here sounds a little like a comment about US economic conditions (though I might be a bit over-tuned, I admit), but in this case it can be seen as a small plus: drugs in the US are now relatively less expensive.

Canada Tightening Hold on Internet Pharmacies

Canda's Health Minister might be trying to strike a fatal blow to the Canadian industry that sells pharmaceuticals across the border to the US.

Health Minister Ujjal Dosanjh may prevent Canadian doctors who do not personally examine U.S. patients from signing prescriptions written by American physicians, a move that could essentially kill the industry. Dosanjh may also create a list of widely used prescription drugs that cannot be exported.

Looks to me like the question of drug reimportation isn't going to be settled by US policy-makers.

December 23, 2004

More DVD Price Wars

Remember that in early October, Netflix raised its price to $22 for it's monthly service, only to have Blockbuster enter at $20. Netflix countered at $18, and blockbuster countered at $17.50. Well, they're still going at it (rr):

How low can you go?I say compare apples with apples: the WM plan for three movies at a time is $17.50--for $15.54, you get two at a time.Like a contestant in a limbo competition, Blockbuster Inc. on Wednesday lowered the price bar for the second time in two months in its war with DVD rental rivals on the Internet.

The video chain slashed the monthly fee for its online subscription service to $14.99 from $17.49, undercutting Netflix's $17.99 rate and the $15.54 charged by Walmart.com, the online branch of retail giant Wal-Mart Stores Inc...

Blockbuster started its online service in August; it has 500,000 subscribers, compared with Netflix's 2.5 million..

Also, while Blockbuster promises 30,000 titles, and Netflix claims 25,000 titles, WM has only 16,000 titles. At the relevant margins, to whom does it make a difference?

December 06, 2004

Oil Price Movements

Via Econopundit I saw this post over at Powerline. Thought it was interesting to look at, so I figured I'd look at a few past years. I've neglected 2003 since Powerline's graph includes some of it, and because the Iraq war introduces an issue that I wanted to sort of skirt around because of time constraints on my end.

Here are the calendar year movements for prices for 2000 -- 2002, all nominal dollars. It's less that I've not got time to adjust the dollars, but more that I was only really interested in the pattern of the movements. (Note: all seasons discussed in terms of Northern Hemisphere -- not meant as a slight to any Southern friends stopping by the site.)

Hmm. That looks a little like we might expect for a seasonal movement in energy. The summer travel season increases demand, while the climb post 11/4/00 might correspond to similar concerns about heating oil supplies we've heard about on the news in relation to current price movements. Possibly a reduction in travel, and potentially the level of oil stocks helped the decrease late in the year.

Summer here is relatively flat. But again we do see that there is some price easing when moving through the late months of the year.

And again a slight increase during the summer into fall, with a reduction in price preceding/entering winter. The difference here, of course, is a marked upturn at the end of the year. Now, what is it that might have occured in late 2002 that made people anxious about oil and oil-producing regions?

The upshot: I'm not terribly convinced that oil prices have moved along with the US campaign for the presidency. Seeing significant movement after controlling for the seasonality of oil prices (that summer is a big time for travel and trasportation -- the biggest sector of oil use -- corresponds to a heated time for the election strikes me as pure conincidence) would do more to sway me towards "conspiracy!!!".

UPDATE: Cite your sources, man! So sorry...all data taken from here.

December 02, 2004

Oil: Stocks vs. Capacity

The recent decline in prices for a barrel of oil seems to be good news for the stock market. No surprise there. But a lot of the commentary in such articles has gotten me thinking. A good deal of the concern is over the stock of oil products. From a WaPo story:

"Oil futures go down, stocks go up. I think that'll be a pattern for a long time, and the good news is that if we keep getting inventory reports like this, oil prices will be ready for a big correction downward," said Brian Belski, market strategist at Piper Jaffray. "Overall, this market has clearly turned to a growth mode over the past few months, and should continue to grow."Stocks of oil and oil products are generally taken as a sign of ability to deliver products on demand when such things as heating oil are needed during the winter. When they're low, the view is that things are getting a bit thin and any unforseen uptick in demand is going to stretch the stocks too far pushing the prices way up. This has been a contributing factor to the recent per-barrel oil prices. From the EIA, here's an illustration of recent stock levels for crude oil:

Sitting at or below average for the first half of the year, then dipping back down again, has helped drive the spot price for WTI up to the levels where it became a campaign issue. So the slide back down can be read as a sign that people have a bit more confidence that our ready supply of oil (as opposed to having to wait for more to be pumped and imported) is going to suffice for the coming months. And, as much as there was a lot of talk about oil reaching new and amazing heights in price, the recent moves have prompted talk of a "correction" to get rid of the "fear premium".

Some of the fear, and thus the escalating prices, is due to political factors in the world. Nigeria had civil disturbances, there were labor strikes in the Netherlands, and Iraq is, well, Iraq. But none of that is really new. We've seen it before, and if recent finds in former Soviet Union countries are any indication, the world will continue to face an oil supply rooted in the world's most unstable regions.

Something I tend to think is under-discussed, at least in the popular media, is the issue of refining capacity. While Saudi Arabia is still the world's swing producer, with the largest amount of excess production capacity (they can turn the spigots on faster and wider than anyone else), having more crude sloshing around doesn't help much if you can't do anything with it. In cases of demand spikes or making up for disruptions in supply, the measurement for being able to smooth over the shake up isn't the amount of oil that can be pulled out of the ground, it's how much oil can be turned into usable things like gas, fuel oil, heating oil, and other distillates.

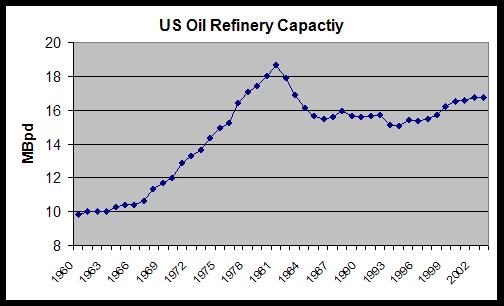

The US hasn't had a new oil refinery come on-line since 1976. Which helps explain this (data from the EIA):

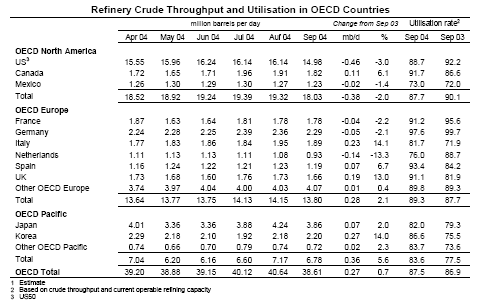

Two things of note, then: 1) the US demands over 20 million barrels of oil a day, and 2) US refineries are running around 90+% of capacity for each plant. This means that, in events like the four hurricanes in the Gulf of Mexico this year (where a large portion of US refining is done) there's little ability for other plants to pick up slack while some refineries are down. And the US isn't the only one pushing its limits. This report from the IEA has one illuminating table (among others):

A number of OECD countries are running at higher capacity rates than the US, especially over the 2003 timeframe. (The US number from Sep 2004 has risen sharply again.)* Since the cost to move crude to the point of refinement is so much lower than the cost to move distillate fuels -- which is why we have refineries here that have capacity far beyond the ability of Texas to pump out oil -- widespread stress on refining capacity means delays in getting products to final distribution to consumer; delays in things like heating oil for the winter (thus the so-far mild temperatures for the winter have had calming effect). Also mentioned in the report is an interesting mismatch between those kinds of oil that are seeing an increase in demand (light/sweet) vs. those that are being pumped out of the ground (heavy/sour). The mix of refineries available to us here in the US isn't well-suited to accomidating such changes.

All this has a direct impact on the stocks of oil, since the refineries are essentially how the stocks get filled. Overtaxed refineries can't react well to interruptions, which means that even small shocks get magnified through the system.

"Oil independence", as it's usually considered, is a pipe dream so long as the US uses oil, and someone, somewhere can pump and ship oil for less than it takes to get it from Texas. But that doesn't mean the US has to be so sensitive to shocks. Having more excess refining capacity (or any at all) might be one way to help smooth things out. Too bad, then, that building new refineries is almost entirely out of the question. The return on investment for refining has actually gotten better, but the regulatory and environmental restrictions (more on the environmental issues here), including nearly 800 permits to secure and reductions of 42% of actual profitability against posited levels without environmental regulations, place it out of reach for any of the "majors". Even if large amounts of capital for investment could be obtained, companies would immediately begin fighting the traditional NIMBY problems of any large industrial facility; it's no wonder US refinery building has gone the way of the dodo**.

And so while it's not entirely certain that high oil prices have a negative impact on the world economy (definitions of "sustained" and 'high", and assumptions about behavior make analyses like this fragile), the addition of refining capacity might be, at least, a hedge against the problems that arise from being so sensitive to fluctuations that are beyond our control.

*Some might notice that I said the US uses over 20 million barrels of oil a day while this chart shows that US refining capacity hit 16.25 million barrels a day. This is how stocks move into the lower edge of the average range, as demand not only surpasses refining capacity but also restricts the amount that can be placed in stocks. Either the US continues to draw down stocks, making the market even more nervous, or the US imports refined products, a relatively expensive alternative.

**Though, unless I'm mistaken, the dodo wasn't regulated out of existence.

UPDATE: My apologies for the misspelling in the "capacity chart". It was a casualty of doing the post over lunch. And, for data about capacity, click here and open the XLS file. The US is up to running around 94% for the week of Nov. 26.

Prices of Gas and Other Liquids

While the price of gasoline has declined for four straight weeks, leading to below the fold reports, fark linked to a comparison of the prices (per gallon) of 46 other liquids along with gasoline.

This type of price comparison, while honestly conducted (except for some goods, which are priced too high), doesn't have any other economic value. At the margin, nobody ever chooses between a gallon of gasoline and a gallon of black inkjet toner and a gallon of mercury; there is no production process where these are substitutes, so the relative prices don't provide any decision-assisting information. They're still cool, though.

October 23, 2004

Proper-Coaseans, the Internet, and Price Discrimination

This weeks Economist has an interesting summary of a paper by Andrew Odlyzko in the Review of Network Economics. The following is the abstract of the paper:

A wide-ranging discussion of the evolution of pricing in early transportation industries, such as lighthouses, canals, and turnpikes, is presented. It shows that price discrimination was an important factor in the development of those industries, and tended to intensify with time. In order to make differential tariffs effective, service providers had the right of detailed inspection of the cargo. These historical precedents help explain the drive by large sectors of the telecommunications industry to gain greater control over what is transmitted over the Internet. The implications for the evolution of the Internet are briefly explored.

As the Economist notes, On England's canals, prices by cargo varied widely by the 1790s, according to both content and ultimate use: for instance, transport was free for manure for adjacent fields and stone for road repairs. To some extent, regulation limited canal operators' ability to exploit their market power: until 1845, they were barred from offering transport service themselves, in a structural separation of the sort sometimes proposed in telecoms today.

History of transport applied to telecommunications, very interesting. Here is another must read paper from the journal on regulatory impressionism (thanks to Knowledge Problem).

October 01, 2004

Moore for Free

Michael Moore has been disinvited to speak at GMU. Sad.

Don Boudreaux notes Moore's dismissal smells politically motivated. I agree, even though Moore's invitation could equally well have been politically motivated.

However, I object to Moore speaking at GMU for a reason Don doesn't mention: Moore is not worth his $35,000 pricetag. I think that the university was overpaying for his services; until Conservatives objected, they were suckers at the bargaining table. And there is at least one person who agrees with me--Michael Moore:

Moore, in a telephone interview last night from his home in Flint, Mich., told The Washington Post he intends to speak at George Mason anyway. "I'm going to show up in support of free speech and free expression," he said.You see, to get Michael Moore at a discount--in this case, a freebie--all you have to do is give him a day's worth of free advertising in the major papers.

A while back, Robert Fisk admitted to a packed GMU crowd that there was no massacre in Jenin; his potent exposure of the injustices of Israeli confiscation of land owned by Palestinians was worth the crowd's attention. If Moore were only half as intelligent as Fisk, it might well be worth it going to see him.

August 28, 2004

Library Book Sales

The Beatley branch of Alexandria (VA) Public Library system sells overflow, discarded, and donated books for 50 cents each. The ostensible purpose of such a low price is to increase the number of books that patrons own and read.

This seems like a great deal for those willing to sort through the junk (an embarrasing assortment of third-rate literature, self-help concoctions, and last decade's programming guides) to find a prize (like I have in Bruno Leoni's Freedom and the Law).

For most of the junk books sold, 50 cents appears to be the going market rate, or just a bit under it, as you can find used copies on Amazon and used bookstores for that price. The library--and everyone else-- are practically giving those books away. There is always a substantial inventory of this pulp, and a rather large turnover. The market in junk books is efficient; economists will sleep soundly.

But for almost all of the good books, 50 cents is way too low to achieve the desired aim of wide readership. In fact, at this price, selling a limited number of good books to interested readers seems to be almost impossible.

The actual result of such a low price is to make it so that expensive books (which are usually the good ones) are almost always out of stock. The price ceiling has created a class of middlemen-speculators who sort through the for-sale shelves, and purchase anything worth more than a few dollars. (I have talked with several of these speculators, and they uniformly won't buy books that they can't sell for less than $3-$4--as the transactions cost of packing & shipping are too high). If they think something is valuable, but don't know its market price, they use the library computers to check Amazon.

Hence, it is mostly the trash that could be picked up cheaply elsewhere that winds up in the hands of regular library patrons. As I wrote above, occassionally I have found books that the speculators didn't realize were valuable, or perhaps I beat them to it, since I arrive just when the library opens.

Frankly, I'm disappointed that Alexandria library is giving a living to unknown persons, instead of selling its books at market rates online. By selling its books, I think it could make enough money to purchase and maintain a wi-fi network, or to buy better books. (I grant that this assumes competency in identifying and selling expensive books, but we're talking about library personnel, who presumably specialize in books).

If the library wants to be a charitable organization that gives valuable books to the needy at a discount, then it should find ways to actually perform this service, instead giving retired persons a means to profit at taxpayer loss.