May 14, 2005

There's a Sucker Born Every Minute

I missed that Argentina had succeeded in a bond offering:

BUENOS AIRES (AFX) - Argentina has issued its first treasury bonds for sale to the financial markets since defaulting on its public debt mountain in 2001, officials saidThis is actually rational since the country is unlikely to default again quickly. However, who's buying these at a 6.5 yield or coupon? Argetina's inflation rate is at least that high and the politicians of the place don't seem to understand monetary economics.The government's bond offering consisted of 1.0 bln pesos, according to finance secretary Guillermo Nielsen

The interest rate was fixed at 6.51 pct annually, but this could be adjusted according to inflation

Nielsen told reporters yesterday's offering was "very successful" and said it showed Argentina was "returning to normal" on the financial markets

April 19, 2005

Nick Leeson Lands a Job

For those you who don't remember who Nick Leeson is, he's the bloke who brought down Barings Bank a decade ago. Apparently, Galway United Football Club has seen fit to have him overlook their books. The LA Times article:

When he interviewed for the job at Galway United Football Club, he said he offered no references and began by discussing the scandal. "The first thing you must deal with is the collapse of the bank and you don't try to put any gloss on it," he said.

This is rather unremarkable, but I want to recommend his book Rogue Trader. His account is highly entertaining with some important lessons to keep in mind. It clears up some misconceptions as to what really brought down the bank. Many times when the incident is mentioned, derivatives trading is the culprit. This is true to the extent that the losses were cause by losses in these instruments. However, these were the result of fraudulent activity on Leeson's part. The only authorized trading his operation was doing was strict arbitrage with another Asian futures exhcange. Rather, the losses were the result of a large error by one of his staff that he attempted to cover up. The Kobe earthquake caused these to explode which he further exacerbated by trading more in the error account.

Most of you probably don't think about your money and securities in your brokerage account and you're safe to an extent. Professional traders actually worry about this a lot( note: I'm refering to certain subclass of traders, from daytraders at prop shops to exchange members/off floor traders. Obviously, a trader at Goldman Sachs has no discretion over stuff like this). Because of the structure of clearing firms, LLCs which are their clients and individual traders, it's entirely possible to wake up one morning and discover somebody at the firm had wiped it out. This could be the result of fraud or poor business practices. This is why most traders don't keep more cash than they have to at their firms. Nick Leeson drives this point home; you never know when his long lost brother might blow up your firm. Like I said, this happens probably more than people outside this certain segment of finance realize.

April 12, 2005

Hedging Options - Bob's New Blog

Although he hasn't asked me to advertise it, I must point out Hedging Options, Robert Arne's new trading blog. Bob is a man who has his priorities straight:

This actually my first trade in a while as I basically took the last six months off from trading. In addition to being a trader, I'm also a Phd econ student. No, they don't mix very well, so I cut back to two classes a semester to focus more on trading.[Emphasis added]One reason I wanted to start this blog is that theren't hardly any options blog out there.

I took a Master's level mathematical finance course a while back, but the whole topic wasn't really exciting to me. But Bob makes it sound like loads of fun!

Here's to econ blog specialization!

April 08, 2005

Day Trading

Undoubtedly, some of our readers have thought of quitting their jobs and becoming daytraders. Of course, I went to graduate school to possibly get away from the vagries of the financial markets if I so desire to at some point. You'll be happy to know if you do choose to quit your job, that your personality doesn't look to play a significant role. From the research paper "Fear and Greed in Financial Markets", the abstract:

The downside is that emotions seem to be significant. Controlling these is far harder than probably anything else. If somebody has ever told you that you have "ice water running through your veins", it may be worth a shot.

We investigate several possible links between psychological factors and trading performance in a sample of 80 anonymous day-traders. Using daily emotional-state surveys over a five-week period as well as personality inventory surveys, we construct measures of personality traits and emotional states for each subject and correlate these measures with daily normalized profits-and-losses records. We find that subjects whose emotional reaction to monetary gains and losses was more intense on both the positive and negative side exhibited significantly worse trading performance. Psychological traits derived from a standardized personality inventory survey do not reveal any specific "trader personality profile", raising the possibility that trading skills may not necessarily be innate, and that different personality types may be able to perform trading functions equally well after proper instruction and practice.

I should say that this isn't new information. Every trader knows this, even I have battled this and still do, but researchers need to publish something afterall. I find it interesting how academics take common knowledge, throw some math and statistics in, and then pat each other on the back for a job well done.

December 31, 2004

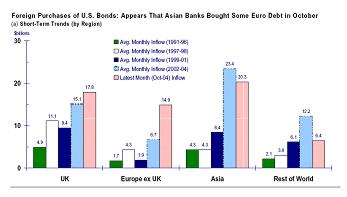

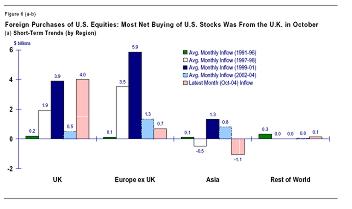

Foreign Inflows in the Bond Market

Brad Stetser had an interesting post that China had started buying mortage back securities. There are some interesting comments following the post, namely one person said that this probably makes a revaluation of the currency less likely since it lengthens the duration of its portfolio.

This reminded me of a chart I saw the other day about foreign inflows into the U.S. The charts come courtesy of B of A Securities' Thomas McManus in a report titled Holiday Shopping(the PDF is behind a firewall). It would appear that that Europe with the exception of the U.K. continues to shun U.S. equity markets, however they seem to find our bond market attractive. So, the falling Dollar vs. the Euro has at least worked part of its magic. Also, anectdotally, I've been told that Europeans are very aggressive right now in the private equity markets. This wouldn't show up in foreign purchases of equities.

The pink spikes are only for October and don't constitute a trend by any means, but it'll be interesting if these numbers hold for the rest of the fourth quarter as the Dollar continued to fall. Interestingly, the U.K. had been heavily investing in the U.S. bond market for the last couple of years even though their interest rates have been higher.

So, while Asia seems to have cut back a little bit on U.S. bond purchases in October, Europe seems to have picked up the slack.

December 29, 2004

Derivatives Blow Up

I haven't seen too many comments of the China Aviation derivatives fiasco around the net. In fact, I don't know how I missed it myself. It looks like last October was a classic short squeeze which coupled with uncertainty surrounding the election drove oil prices to their highs. The story is that the firm lost $550 million partially due to rising oil:

Singapore has arrested the chief executive.

The oil-trading company said last week it ran up losses as crude-oil prices surged to a record $55.67 a barrel in October.``Financial difficulties of the company are due to trading losses and critical cash flow problems as a result of its losses in the trading of derivatives and the requirement to place margin deposits with counter-parties as a result of the losses,'' Chen said in an affidavit filed with Singapore's High Court on Nov. 29.

China Aviation first reported the transactions to its Beijing-based parent, China Aviation Oil Holding Co., on Oct. 10, Chen said in the affidavit.

Also under investigation is the sale of a S$196 million ($120 million) stake in the company by its state-run parent in October. The sale, managed by Deutsche Bank AG, was to raise funds to cover margin calls, or demands for funding, on the company's derivative positions, Chen said in the affidavit.

There are always rumors whenever there is a sharp rally in any market that somebody is on the wrong side and is about to blow up. Undoubtedly, they probably aren't the only ones who suffered steep losses.

December 17, 2004

Yukos "Hail Mary" Bankruptcy Filing

The last ditch attempt by Yukos managers to fend off a forced Russian "auction" of its assets to Putin-controlled Gazprom seems to have worked--for now, anyway. Frankly, this is incredible and amusing in a dark sort of way:

A Western bank consortium led by Deutsche Bank has frozen a planned credit line to Gazprom following a U.S. bankruptcy court injunction against the sale of the Yukos oil company's main subsidiary, the ITAR-Tass news agency reported Friday.Of course, since Gazprom will be the only offer actually considered by the Russian authorities, does it really matter if their financing fails? I mean, a rubber stamp is a rubber stamp. This is just a nationalization program orchestrated to fit into globalization rhetoric:Gazprom, the state-controlled gas giant, was the expected buyer of the Yuganskneftegaz unit, which produces about 60 percent of Yukos' oil, at the auction scheduled for Sunday. The credit line is thought to be worth $10 billion.

Freezing the credit line could effectively prevent Gazprom from bidding unless it found alternative financing.Citing unidentified, high-ranking Western financial sources, ITAR-Tass said the banking group had decided to freeze the deal at least until the bankruptcy court in Houston reaches a final decision.

One of the sources quoted by ITAR-Tass said the move was necessary, ``because in case a credit line is given to Gazprom over the next 10 days, Western banks would risk falling under legal prosecution in the United States.''

A ruling late Thursday in a federal bankruptcy court in Houston, however, raised some questions about the participation in the auction of banks that were expected to finance the deal. A federal bankruptcy judge in Houston, Letitia Z. Clark, issued a temporary restraining order intended to block the participation of lenders and Gazprom. The banks, analysts said, have extensive operations in the United States and might be concerned about ignoring the restraining order, which could put them in contempt of court.Well, duh?!? I'm disappointed, but not surprised, that U.S. newspapers give the Russian government'sBut Judge Clark's ruling did not apply to the government of Russia, and analysts said they expected the Russian authorities would go ahead with the auction on Sunday regardless of the ruling....

Although two other largely unknown companies have submitted bids for Yukos in the auction, their presence was seen as purely an effort to make the auction seem valid. Foreign investors, including companies from China, India and other overseas energy investors, have been discouraged from participating.

UPDATE:The FT joins the fray:

There is yet another scenario: namely that the Russian government proceeds with Sunday's auction, to demonstrate its independence from US law - but this auction then fails because Gazprom cannot get funding to meet the official $8.6bn sale price. If that occurs, the state may then seize control of Yugansk and subsequently sell it to Gazprom at a considerably lower price. There is no proof that this is what the government plans. That scenario might yet suit the Kremlin rather well. In the meantime - and as conspiracy theories swirl - the one thing that is clear is that the potential legal risk for Western bankers is rising by the day.UPDATE 12/18: The drama continues with a $9.3 billion sale to an unknown company:

Virtually nothing is known about the winner, BaikalFinansGroup, which emerged as a bidder at the last minute -- after a U.S. court issued an injuction against the auction, disrupting plans for a bid from the company that had been seen as the Kremlin's favorite to snap up the unit: the state-controlled natural gas behemoth, Gazprom.Observers, however, believe BaikalFinansGroup could be just an alternative vehicle for Gazprom, with sources of funding that are different from those initially prepared.

Stephen Dashevsky, a leading analyst for Russia's Aton brokerage, said the winner was likely affiliated to Gazprom.

ITAR-Tass news agency claimed that BaikalFinansGroup's registration address -- in the central city of Tver -- corresponded to that of one of Gazprom's structures.

Gazprom said Sunday that neither it nor Gazpromneft -- its oil component, which was officially making the firm's bid -- had any relation to the winner, the Interfax news agency reported.

UPDATE 12/20: Can you believe that people are suspicious that the sale of Yukos was just hanky-panky? But, hey, Russia is a normal country, no?

The auction on Sunday seemed reminiscent of Russian privatization deals in the early 1990's - with murky financing, questionable bidders and unknown companies representing powerful financial groups emerging to win lucrative assets. Many of Russia's current generation of new oligarchs became billionaires in those deals overnight.UPDATE 12/21:Russia's de-facto dictator Putin reveals some more details:"This bid by Baikal Finans Group was a smoke screen and a delay tactic," said James Fenkner, head of research at the brokerage firm Troika Dialog - possibly, he said, to allow Gazprom more time to raise funds. "Why can't there be a transparent auction run by the state? The whole thing just makes Russia look bad."

The Baikal Finans Group, which listed its address as the same as that of a cellphone store in Tver, won a controlling stake, or 76.79 percent of the shares, in Yuganskneftegas with a bid equivalent to about $9.35 billion. That was above the starting price of $8.65 billion, but still far below what is considered he fair market value of the unit, according to independent banks hired separately by Yukos and the Russian government.

It is possible that another Russian oil company with lots of cash, like Surgutneftegas, was the real bidder, but analysts said it was more likely that all this was a way to give Gazprom time to come up with new financing.

The Russian government's prosecutorial assault on Yukos and its founder, which began in summer 2003, has set foreign investors on edge and raised questions about the rule of law, property rights and President Vladimir V. Putin's commitment to economic change. And Sunday's blow to Yukos, which had already sought bankruptcy protection in Houston last week, seemed part of that pattern.

The bidding process for Yuganskneftegas was a bizarre, confused affair: reporters were invited to watch the afternoon auction at the Russian Federal Property Fund's offices, but only on big-screen television sets. The property fund did not provide any information about the bidders.

Officials of Gazpromneft and the Baikal Finans Group sat side by side at separate tables in a plain, brown and beige room. Baikal made an opening bid, and then a Gazpromneft official left the room briefly to take a phone call. He returned a few minutes later, but Gazpromneft never submitted a bid.

The Baikal Finans Group's representative again raised his paddle, winning with a bid of 260.753 billion rubles, or almost $9.35 billion. From time to time, he conferred with a colleague sitting next to him. After just 10 minutes of bidding, the Russian Federal Property Fund, which organized the sale, announced Baikal Finans Group as the winner.

"The shares have been sold," said Valery Suvorov, a deep-voiced auctioneer dressed in bowtie and tails and wielding a gavel....

If Baikal should fail to make full payment for the Yuganskneftegas assets in the 14-day period required, under Russian law the government can order a new auction or seize Yuganskneftegas in lieu of unpaid taxes.

Russia's other major oil companies - including, besides Surgutneftegas, TNK- BP and Lukoil - all denied any ties to the Baikal group, according to the Interfax news agency.

"The shareholders of that company are exclusively private individuals," Mr. Putin said in remarks televised from Germany, where he is on an official visit. "But they are individuals who have for many years engaged in the energy business."Mr. Putin further hinted that the new owners would not have, or maintain, exclusive control over their rich new holding, as industry analysts had speculated.

"As far as I know, they intend to establish certain relationships with other Russian energy companies which may be interested in this asset," he said.

Speculation has swirled around the identity of the buyers of Yuganskneftegaz, the Yukos subsidiary, since it was purchased at a six-minute auction on Sunday by Baikal Finans Group, a company that had not been heard of until days before the sale....

In an interview in the Komsomolskaya Pravda newspaper published today, Viktor Gerashchenko, chairman of the Yukos board of directors, summarized the Yukos position bluntly: "On Sunday they sold stolen property," he said.

Asked who it had been stolen from, Mr. Gerashchenko was equally blunt "They stole it from us," he said. "And they sold the company producing 20 percent of the country's oil to God-knows-who."

UPDATE 12/22: Thomas Barnett has a nice one-phrase summary:

Nye sluchaino chto is a wonderful old Russian phrase that means, "It is not by accident that . . ..Indeed.

UPDATE 12/23: Rosneft just bought Baikal, and Putin insists that the sale of Yukos was "perfectly normal". :

President Vladimir V. Putin of Russia today strongly defended the purchase by a state-controlled company of the winner of Sunday's auction for the largest subsidiary of the oil giant Yukos.What a dishonest, pathetic man--even by the standards of politicians. The sale of Yukos was a complete sham."Today, the state, using absolutely legal, market mechanisms, is ensuring its interests - I consider this perfectly normal," Mr. Putin told reporters at a news conference in Moscow, referring to the purchaseby Rosneft of the Baikal Finans Group, which had widely been thought to be a shell company.

Mr. Putin talked of how the oligarchs, or private businessmen, obtained properties at bargain basement prices soon after the breakup of the Soviet Union in 1991.

"Some market participants got multibillion state assets using different tricks, including some violations of then-existing legislation," Mr. Putin said.

By contrast, he said, the purchase by Rosneft "was done in absolute conformity with market means."

With the purchase complete, Rosneft is scheduled to merge sometime next year with Gazprom, Russia's natural gas monopoly, which had widely been thought to be the government's choice to win the auction in the first place....Rosneft stock is growing since it bought Baikal:Rosneft did not reveal what it paid, but Yuganskneftegas had been valued at $14 billion to $22 billion.

On Sunday, Baikal paid about $9.35 billion for 76.6 percent of the shares in Yuganskneftegas.

"Owners of Baikal Finans Group offered Rosneft to buy their assets, obtained through the sale of Yuganskneftegas on Dec. 19," a Rosneft official in Moscow told the Interfax news agency. "Rosneft bought 100 percent of shares previously owned by Baikal Finans Group."

Moscow. (Interfax) - The shares of Rosneft subsidiaries have been growing rapidly at Moscow's MICEX exchange following reports that Rosneft, Russia's state oil company, bought 100% of shares in Baikal Finance Group, a company that bought 76.79% of shares in Yukos's principal production unit, Yuganskneftegaz, at a Sunday auction.Forbes has more:Rosneft-Purneftegaz common shares gained 13% in their value to 667 rubles from 590 rubles in 5 minutes of trading at MICEX. Its preferred shares rose in price by 9.8% to 450 from 410 rubles.

Rosneft-Sakhalinmorneftegaz common shares grew by 7.7% to 160 from 148.52 rubles, and its preferred shares by 8.6% to 115 rubles from 105.88 rubles.

Russia did not grab the company by force of arms or through eminent domain. If it was a power grab, it was done through a series of steps, each one at least putatively legitimate: enforcement of tax and fraud laws, foreclosure on tax liens, an auction of assets for which $9.4 billion bid was paid (showing at least some concern about the rulings of a U.S. bankruptcy court) and a sale of the assets to a richer entity. The scenario suggests a consideration for the rule of law (or at least a concern for appearance) that would have been surprising in Russia just two decades ago.Also, it is completely true that the oligarchs used connections to obtain state assets at huge discounts off market prices. Putin is using his state power to do the same with market assets...

Along those lines, Lynne Kiesling makes a bold understatement:

This retrograde development sends a chill up my spine. Using the heavy hand of the state to punish someone for buying Soviet assets at the post-Soviet fire sale, and then re-nationalizing them at a discounted price and still claiming it's all market-based and open and aboveboard. I am totally not convinced.

November 29, 2004

Private Equity

The Economist has a survey of private equity this week(only one of the articles is free). It raises many of the points that a friend of mine who works for one such firm has been making for a couple of years now. Here's an excerpt, but read the whole thing(my friend even gets comments comparing him to the portrail in movies):

Will tougher competition and increasingly demanding investors cause the industry to consolidate? Sir Ronald Cohen of Apax Partners thinks that over the next decade the private-equity industry will polarise. At one end, a few big global industry leaders will emergemaybe three or four dominant brands with high returns; at the other, small specialist firms will thrive. In the middle, however, many firms will find it hard to compete. His prediction is plausible, and the losers may include some famous names. Forstmann Little has already said that it will close in 2006. It made some awful telecoms investments during the bubble and has failed to resolve its succession problem.

July 20, 2004

Dividends are Gifts?

The summaries of New York Times articles on the front page are sometimes wildly off the mark, like the summary for this one:

UPDATE (7/21, 10:44 AM): It seems the Times web editors have had a change of heart:

June 23, 2004

Going Dutch Souring Prospective Partners?

Google's much ballyhooed Dutch auction IPO might not be to the liking of some serious institutional investors.

The exit of Merrill, one of the country's largest brokerages, from involvement in Internet innovator Google's highly anticipated and equally unusual IPO (see full story) may lead others to decide that the rewards don't measure up to the required investment of time and money.

Link in original story.

Of course, I doubt Google's too worried about that. They don't seem like the types to be scared off their plan by the huffing and puffing of the big players.

June 07, 2004

More Credit Rating Agency Issues

Last week, I posted an article from International Economy. Appearantly, the mood to examine the credit ratings agencies have spread to this side of the Atlantic, but unlike in Germany the impetus has been ratings users(oops, forgot the link, here it is):

Credit rating agencies might be required to submit to new record-keeping and reporting requirements when the US Securities and Exchange Commission, the US financial regulator, concludes its long-running review of the industry.

The move would be the most significant reform of the ratings business in decades and would give the SEC greater authority to examine how the agencies assess companies' creditworthiness, according to people close to the regulator.However, it is unlikely to be welcomed by some credit rating agencies, which regard tighter controls of their lightly regulated sector as unnecessary.

But in an apparent concession, the SEC is not expected to make significant changes to its system of officially recognising certain agencies.

The designations of "nationally recognised statistical ratings organisations" is held by only four agencies: Moody's Investors Service, Standard & Poor's, Fitch Ratings and the Dominion Bond Rating Service. However, eligibility guidelines for entry to this elite could be clarified. Formal action by the SEC is expected by the end of the year.

Scrutiny of the ratings industry increased following the collapse of energy trader Enron in late 2001. Congress convened special hearings and demanded to know how the agencies could have rated Enron as a creditworthy risk days before it imploded.A year ago the SEC issued a report outlining a range of possible reforms, including introducing "more pervasive" regulations.

Under the current system, the SEC holds informal meetings with the agencies only every few years and does not evaluate how they reach decisions.

Investors, however, have been telling the SEC they want more transparent information about how the agencies assess creditworthiness. The Investment Company Institute, an association of m utual funds, has recommended the regulator require agencies to maintain records of their decision-making.

Fidelity Investments, a mutual fund, has suggested the agencies disclose the date and location of their most recent meeting with the management of debt issuers.

The ratings agencies declined to comment on SEC's review. Moody's said: "We're engaged in conversations with the SEC and are co-operating fully."

But some have indicated they would be unhappy with any regulations that intrude too deeply into their business operations.

S&P said: "We would consider record-keeping requirements in light of our current practices, the fact that ratings are not investment advice and our First Amendment protections."

The SEC declined to comment.

June 04, 2004

Google IPO

A CBS MarketWatch article points out the weariness that fund managers have about the Google IPO. Much of it sounds like snivelling that they have lost their advantage over retail investors:

They don't like the sounds of getting in at a price they can't make money off of. They fear the price they'd be receiving isn't much of a discount than what retail buyers would get.It's akin to bypassing the high mark-ups you'd get from Pottery Barn, Saks or any retail outlet for that matter. Where's the value for such middlemen retailers? If Google were a new brand of wildly popular jeans sold at the same price to both consumers and retailers, then retailers might opt to buy cheaper imitations or jean jackets they can offload to consumers at higher prices.

In like vein, fund managers are finding alternative investments to play the positive sentiment surrounding the IPO.

To be sure, some fund managers expect the Google IPO to be the top of the Internet market. They'd look to short most Net shares. But I would argue that Google planned its IPO well.

I would say that Google planned its IPO well to extract as much money out of the market as possible. Initial trading of the stock is likely to be down which is contrary to how most internet stocks traded in the late nineties. The reason is simple; who is left to buy at that price? If the hesitency of fund managers to participate is widespread, it is conceivable that it may open lower than expected and institutions may jump in at that point. I think that's unlikely to happen and that individuals are likely to bid up the IPO price. There is something in the market called 'natural selling' which means that there is always somebody out there holding a stock who needs to paint the garage or pay for their daughters wedding. This phenomenom is why in slow markets, it seams stocks like to drift down. I find this much more common in smaller stocks who don't have much coverage. So, if you're planning to participate, I recommend a low ball bid.

May 31, 2004

Credit Rating Agencies

I was reading this past winter's The International Economy and read an article called, "Das empire strikes back: German banks have had enough of Standard and Poor's and other agencies, and they're not going to take it any more." I cringed reading this(no link since the article isn't available on the mag's site):

For more than a decade, bankers, industry executives and politicians on the Continent have complained about Europe's humiliating dependence on the almighty U.S.-regulated rating oligopoly. Now, the revolt against America's unchecked rating power is pressuring politicians to push the European Union towards regulating the global rating trio. There is a groundswell of support for establishing a European rating agency. But all this is easier said than done.As European companies move from borrowing money from their banks to tapping the world's capital markets directly--by issuing bonds, medium-term notes, or commercial paper--their securities need to be rated. But there is a problem: Europe doesn't have a major rating agency that would take into account the special characteristics of European accounting or the prevailing differences in financial ratios as they evolved in a bank-based financial system.

Finally, this problem is becoming political. Proposals by the European Parliament's Committee on Economic and Monetary Affairs to establish a European Registration Authority for rating agencies under the auspices of the Committee of European Securities Regulators (CESR) may be far ahead of the curve. They point to "a European nightmare--that unchecked American rating agencies become the Continent's boss men." EU parliamentarians are looking for ways to contain American rating power by putting global rating giants like Standard & Poor's, Moody's, and Fitch under some kind of new EU regulation. So far the Brussels Commission--with the British government keeping a watchful eye on the stakes for London as a global financial center--is playing for time. But the German government, faced with a domestic revolt against damaging rating decisions by Standard & Poor's, is under mounting pressure to control what is perceived as an excessive level of American rating power.

Then I found it amusing. Why does everything have to be humiliating? Overall, it's a pretty good read; the Germans may have an issue or two, but what if they regulate the agencies to irrelavency? For all the sniping from Europe when Worldcom, Enron and so forth happened, European business is more convoluted and the relationship between them and government is cosier. What if they mandate an unsound business practice because it's a local common practice? Of course, when they say American firms don't understand Europe, they have a point; large companies inevitably get bailed out in some form or another, so why bother with ratings at all. If you click below, the guarantees going to the Landesbanks merely turn from explicit into implicit, in my opinion.

edit: A visitor posted an interesting comment, click to read.

By announcing, on November 13, 2003, that it would come up, by November 24, with down-grades on unguaranteed Landesbank obligations, Standard & Poor's was set to deal a fatal blow to an important sector of Germany's banking system, the Landesbanks. This is why. Under an agreement with the EU Commission in Brussels, eleven Landesbanks must phase out state guarantees by July 18, 2005. This is considered an important step toward securing a level playing field in European financial markets. The Landesbank guarantees have supported top-notch credit ratings, which in turn meant cheap funding. Critics charged that by publishing Landesbank ratings on the basis of unguaranteed obligations immediately, i.e., long before the phase-out of state guarantees in 2005, Standard & Poor's was unsettling the difficult phase-out process. Indications from the "unguaranteed debt" ratings that were leaked following the announcement on November 13 suggested that all but three Landesbanks would be allocated ratings in the BBB--range, compared with the AA and AAA ratings they currently receive. What a blow.To large segments of Germany's political and financial establishment, Standard & Poor's rating action amounted to a declaration of war. It was noted in German official and business circles that Moody's, the other major U.S. rating agency, distanced itself from Standard & Poor's bombshell. Juergen Berblinger, managing director of German operations for Moody's (who left at the end of 2003), indirectly criticized his competitor's rating action by stating: "In our view it is inappropriate and premature to publish unguaranteed ratings." He was supported by Moody's veteran European bank analyst Samuel Theodore, who sharply criticized Standard & Poor's move toward publishing notional ratings. Fitch, the smaller rater, first kept its powder dry by signaling that it would only put out ratings on an unguaranteed basis in case the Standard & Poor's went ahead with their announced notional ratings. When it became clear that Standard & Poor's had reversed itself and announced that it would publish their unguaranteed ratings about half a year later, Jens Schmidt-Burgel, head of Fitch in Germany, followed suit by telling the press, "It's clearly the wrong time to publish such ratings."

There was unprecedented political pressure exerted by the German government, financial supervisors at BaFin (the German Financial Supervisory Authority), and the Bundesbank on Standard & Poor's not to publish those "notional" or "fictitious" ratings. They argued that it was much too early to do this. Parallel ratings would unsettle the difficult transition process between now and the middle of 2005. Such ratings would not adequately rake into account the fact that all obligations issued by Landesbanks expiring before 2015 would be covered under the state guarantees.

As was to be expected, German banking associations representing the Landesbanks and their main shareholders, the Sparkassen, mounted a fierce counter-offensive. Argues Karl-Heinz Boos, executive managing director of the Bundesverband Offentlicher Banken Deutschlands (VOB): To issue notional ratings at this time when most Landesbanks are in the process of adjusting their capital base and business plans is "irresponsible and unprofessional." High officials in the Berlin finance ministry reacted angrily: Should Standard & Poor's issue parallel ratings (with and without guarantees), this would mean that the lower ratings would stick to obligations even if these were covered by state guarantees--which damages the is suing bank. Edgar Meister, the Bundesbank's banking supervisor, told a press conference: "These notional ratings are not particularly appropriate for evaluating a situation that won't be here until 2005. We should grant the Landesbanks time to adapt and implement their strategies. Publishing such ratings could make this more difficult."

And Jochen Sanio, Germany's chief financial supervisor, told Handelsblatt, Germany's business and financial daily, that he "cannot see any valid arguments that Standard & Poor's could put forward to justify fictitious ratings for Landesbanks at this time." Sanio sees today's major rating agencies as "uncontrolled world powers that are directing global capital flows by appraising the credit standing of debtors." And pointing to the bitter fight of German corporations against Standard & Poor's downgrades because of differences in accounting for pension liabilities, Sanio warns: "It is simply not acceptable that corporations have no way to defend themselves in important accounting disputes by appealing to an independent authority." Therefore, Sanio argues, "European corporations should think seriously again of supporting a European rating agency that in its initial phase could get additional credibility by putting itself under a financial supervisory agency." And he warns: "Until now rating agencies have been able to operate without being forced to adhere to generally recognized or binding principals. This cannot go on." Although rating agencies have not been brought under financial supervision so far, one should expect that they adhere to the highest ethical standards, says Sanio.

The downside to fighting back:

When an empire strikes back, there are winners and losers. On November 24, Standard & Poor's had to scrap plans for the highly contested rating down-grades of the country's public sector banks in a move, says the Financial Times, "that sent worrying signals to investors." Without giving names, the Financial Times quoted prominent bankers at Germany's Landesbanks warning that "political attempts to influence rating agencies' plans for the sector could be catastrophic for the country's reputation in financial markets." The paper quoted another banker from the state bank sector: "There are only losers in this, as far as reputations go: Standard & Poor's has egg on its face and we are left with uncertainty hanging over us."Giving in to heavy political pressure, Torsten Hinrichs, head of Standard & Poor's in Germany, gave the state banks a year more of breathing space. He came out with a statement that, "Standard & Poor's has decided not to publish the preliminary ratings on individual banks at this point in time because the Landesbanks are still in the process of determining and developing their structures, strategies, and plans to cope with a new environment after the loss of state guarantees in July 2005." Instead, Standard & Poor's will publish the ratings on the Landesbanks' unguaranteed obligations in July 2004, one year prior to the loss of the state guarantees, on which the current ratings are based.

"Standard & Poor's has reached this decision based on the fact that many of the banks' plans are still a 'work in progress', involving fundamental decisions regarding the banks' future business models, restructuring plans, closer cooperation with the savings banks, intra-group support mechanisms, and ownership structures," says credit analyst Michael Zlotnik. But Standard & Poor's made sure to get the eleven Landesbanks working on their stand-alone ratings by announcing that "following the completion of its review of the preliminary ratings on the unguaranteed obligations of German Landesbanks ... it has determined that the ratings on such obligations from today's perspective would range from A+ to BBB." This raises the obvious question: Didn't they know this all before?

However, in the view of Achim Duebel, a veteran World Bank financial sector expert, an argument can be made in favor of stand-alone ratings. When, in 2000, Fannie Mae and Freddie Mac agreed with the U.S. Congress to solicit such stand-alone ratings, this resulted in greater transparency of the implicit guarantee given by U.S. taxpayers to these institutions. Similarly, German taxpayers are entitled to see the dimensions of support they are giving through the guarantees to the Landesbank sector. By looking at the difference between the two ratings--with and without the guarantee--the cost of the guarantee can be quantified. In the case of Fannie Mae and Freddie Mac, the stand-alone rating action had no noticeable impact on the spreads of the debt they issued.

More people who don't want to overdue regulation:

The umbrella organization of Germany's banking association (Zentraler Kreditausschuss, or ZKA) has asked the German government to push for an international regulation of rating agencies with an eye towards minimum requirements for harmonization. In this effort Germany should build on recent work done by the SEC. Pointing to the 95 percent market share of the three rating agencies, the ZKA warns European financial supervisors, government officials, and legislators to stop linking more and more regulation to ratings thereby further increasing the dominance of the U.S.--regulated rating duopoly.